Developing a Global Financial Trust Index

Summary

The proposal is to create a Global Financial Trust Index (GFTI) in order to inform debate on financial trust issues, such as financial crime or money laundering, and to provide a longer-term metric for analysis. GFTI is analogous to two other equally successful indices with similar aims already produced by Z/Yen in different domains – the Global Financial Centres Index (GFCI) and Taylor Wessing’s Global Intellectual Property Index (GIPI). Both are available online –http://www.zyen.com/activities/gfci.htmland http://www.zyen.com/activities/global-intellectual-property-index-gipi.html.

This outline proposal is intended to widen discussion, to initiate support and to provoke thoughts for improving either the GFTI or its potential impact.

Objectives & Scope

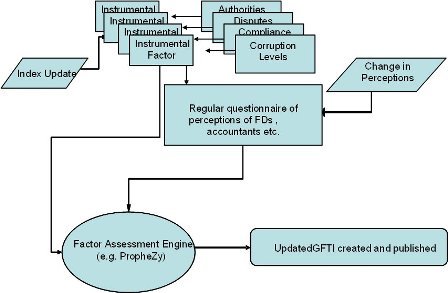

The Global Financial Trust Index (GFTI) would provide ratings of different countries by how ‘trustworthy’ the business-financial environment is. The GFTI would be calculated by a ‘factor assessment model’ built using two distinct sets of input:

- instrumental factors - drawn from external sources, for example, levels of corruption could be indicated by ‘instrumental factors’ such as the Corruption Perceptions Index by Transparency International, the Opacity Index by the Milken Institute and the Ease of Doing Business ratings by the World Bank. Not all countries will have data for all instrumental factors and the statistical model would take account of these gaps;

- respondent assessments – to construct the GFTI ratings we would use assessments drawn from respondents to an online questionnaire. The online questionnaire would run continuously to keep the GFTI up-to-date with people’s changing assessments.

Every time new assessments arrive, or instrumental factors change, the index can updated, though we would probably suggest issuing GFTI half-yearly. Z/Yen would research the instrumental factors, compile them, survey respondents, analyse the data and produce a report suitable for publication.

Approach & Methodology

The respondent assessments and instrumental factors are used to build a predictive model of country trustworthiness using support vector machine (SVM) mathematics. The SVM used for building GFTI would be PropheZy – Z/Yen’s proprietary system. SVMs are based upon statistical techniques that classify and model complex historic data in order to make predictions on new data. The SVM used for the GFTI would provide information about the confidence with which each specific classification is made and the likelihood of other possible classifications. The predictive model provides the overall index by answering questions such as:

If a Munich-based ACCA member gives USA, Germany, Malaysia and the UK certain assessments then, based on the instrumental factors for USA, Germany, Malaysia and the UK, using the factors for Australia, how would that person assess Australia?

We would propose developing sub-indices around the different categories of respondent – for example, how are different countries assessed by finance directors, practicing accountants or accountants in public service. Further discussion on who might be included in the GFTI survey is needed.

The process of creating the GFTI is outlined diagrammatically below:

A few features of Z/Yen’s factor-assessment approach are worth noting:

- every time an input survey is updated, there will be adjustments to the attractiveness ratings without needing to re-survey people in financial services globally, and the adjustments can generate news;

- people’s impressions change the ratings and can generate news almost continuously, if enough people are regularly cataloguing their perceptions;

- there can be multiple inputs to each of the factors, e.g. competing tax inputs, thus keeping up interest, providing alternatives and generating ‘sub-news’ such as FATF’s effect on offshore financial trust;

- GFTI can develop a club of organizations providing relevant competitiveness/attractiveness indices such as the large professional services firms or trade bodies;

- GFTI can develop a club of ‘raters’, i.e. people who don’t mind being surveyed, say, quarterly – thus a club of individuals supporting ACCA in developing its views;

- sub-indices cab be developed without much effort by categorizing people into groups such as legal, buy-side, sell-side, insurance, re-insurance, banking, commerical. This would make it easy to rate Hong Kong as trustworthy in wholesale brokerage (for instance) while less trustworthy in reinsurance (for instance);

- over time, as confidence builds, the factor model could be queried in a ‘what if’ mode, for instance “how much would Chinese prosecution times need to fall in order to increase China’s ranking against Mumbai?”

Creating the GFTI does not involve just totalling or averaging instrumental factors, rather a statistical multi-variate correlation of perceptions with facts. An approach involving totalling and averaging contrasts with Z/Yen’s factor-assessment model as follows:

- indices are published in a variety of different forms: an average or base point of 100 with scores above and below this; a simple ranking; actual values; a composite ‘score’;

- indices would have to be normalized, e.g. in some indices a high score is positive while in others a low score is positive;

- not all countries are included in all indices;

- indices would have to be weighted centrally, rather than by respondents’ perceptions.

Instrumental Factors

We would research factor inputs of financial trustworthiness from external sources. Where indices are already in the public domain, we credit the relevant organisation as the source of the data. There may be organisations that have conducted relevant research, but who do not publish their data, for example PwC’s provision of special tax data for GFCI. Additional data might be obtained at a cost but we believe that there is likely to be sufficient publicly available data for the GFTI without the need to buy additional information. A number of the instrumental factors used in creating the GFCI could be incorporated within the GFTI as they bear on financial trust, for example:

- Administrative and Economic Regulation, OECD

- Ease of Doing Business Index, World Bank

- Opacity Index, Kurtzman Group

- Corruption Perceptions Index, Transparency International

- Index of Economic Freedom, Heritage Foundation

- Economic Freedom of the World Index, Fraser

- Political Risk Score, Exclusive Analysis

- Global Legal Service Centres, GaWC

- Economic Sentiment Indicator, European Commission

- World Competitiveness Scoreboard

- Global Competitiveness Index, World Economic Forum

At the outset of this project, we would agree guidelines for instrumental factors. These guidelines would ensure that instrumental factors were selected and used in a way that will generate a credible, dynamic rating of the trustworthiness of business environments around the world.

Respondent Assessments

The guidelines for assessments by respondents might be:

- responses are collected via an online questionnaire which runs continuously. A link to this questionnaire would be emailed to the target list at regular intervals and respondents would have an ‘account’ where they could update their thoughts;

- the GFTI would be compiled using all assessments from the previous 36 months, weighted dependant on when the assessment was made;

- initially all responses would be included in the GFTI model. As the GFTI is established, a semi-stable list or ‘club’ of regular respondents would be developed;

- the number of assessments from any country would be regulated to ensure good representation of all countries in the GFTI.

Assessments would be included in the GFTI model for 36 months after they have been received. Responses would be given a reduced weighting by age on a log scale.

Online questionnaire

The questionnaire should be brief to encourage a good response rate. The questionnaire would be aimed at finance, accounting and tax professionals (and potentially other groups of professionals) from as wide a range of countries as possible. The key issue is that these respondents should provide a good representation of countries. We recommend that the online web-based questionnaire be conducted continuously, but with a ‘recruitment drive’ twice a year.

Next Steps

This note is designed to initiate conversation. Z/Yen is interested in exploring these issues further with all parties. Please contact Michael Mainelli, Director, Z/Yen Group Limited, Michael_Mainelli@zyen.com