IndeZy ‑ Market Indices For Wholesale London Insurance ('model contract indices and benchmarks')

Call for Participation - January 2008

Background

IndeZy is a proposed project to evaluate the feasibility of establishing price indices and process benchmarking in wholesale insurance. The basic proposed approach is to use model contract indices and benchmarks.

The London wholesale insurance market lacks a vital ingredient, public price information. Markets consist of people trading something with each other and some evidence of prices. In the London insurance market brokers and underwriters trade, but the market lacks clear price signals and is, consequently, rather opaque. This opacity diverts business from London.

The insurance industry is under increasing cost pressure and regulatory pressure. Clients seek evidence that the industry is genuinely cost competitive. Regulators want assurance that market reforms are working. More authoritative evidence would come from prices that in turn forced more rigorous benchmarking of processes and costs.

In contrast, the investment banking sector is price rich and over the past decades has developed several process benchmarks managed by Z/Yen Group (Z/Yen). There are global Z/Yen cost/transaction benchmarks on equities, derivatives, FX and money markets; quality benchmarks on the operational performance of brokers (the sell-side); and process benchmarks on the operational performance of clients (the buy-side). Can we have similar prices and benchmarks in insurance?

Index Services

A great opportunity beckons, indices for policies and claims. If the insurance industry had reliable indices, then capital markets could use those indices to provide tradable markets for policies and claims. Tradable markets in policies and claims would allow customers to hedge and underwriters to improve the use of their balance sheets. For example, a large marine or aviation customer (shipping company, airline) could hedge against a rise in policy costs next year. An underwriter might want to hedge against a rise in claims, thus reducing regulatory capital requirements. Indices would permit an enormous, liquid market in price movement making the insurance industry more profitable and safer.

There are significant movements in insurance prices, and thus opportunities to provide hedges against those price movements. An insurance hedge would be of interest to:

- finance directors of large corporates who wish to control insurance cost volatility;

- reinsurers who may wish to hedge price movements across periods;

- brokers/underwriters who wish to offer options, perhaps for a limited period of time, on policies;

- finance directors of insurers seeking to optimize regulatory capital requirements;

- brokers/underwriters trying to hedge returns on new product launches;

- investment bankers seeking to stabilise prices in deals.

However, insurance prices are difficult to express simply. Policies contain specific clauses and exceptions; they are not commodities. What is needed is a trustworthy index that gains acceptance as a valid indicator of true prices over time.

Indices would need to be offered class-by-class for policies initially and later for claims. There would be a taxonomic tree of standard contracts ('model contracts'), e.g. a 5,000 tonne marine hull, a Y tonne hull, likewise similar standard contracts in aviation, etc. After indices gain acceptance, then products such as forwards, puts and calls can be offered against the index. The long-term model is to charge for services such as:

- licensing to launch products linked to IndeZy indices;

- data sales;

- alert services;

- news feeds;

- advertising placements.

Benchmarking

Entire books have been written on benchmarking but, in a nutshell, benchmarking is a process comparing two or more business processes in order to understand how to improve them. Processes can be compared within an organisation (e.g., a multi-national contrasting finance processes in subsidiaries in different countries) or among different organisations (e.g., a club of companies sharing information on their finance processes). Good benchmarking has been the starting point of many successful change programmes. Equally, poor benchmarking has scuppered change programmes or has overlooked opportunities for improvement.

Organisations obtain benefits of many different sorts from benchmarking:

cost reduction and quality improvement: by understanding where your organisation stands on cost/transaction and process turnaround, you get an overall measure of performance and an indicator of where effort should be placed, e.g. cost-reduction or quality-improvement;

- new levels of performance: learning about other organisations expectations in order to set your own. One investment bank with which Z/Yen worked set about contrasting their product control with internal audit, sparking a healthy internal competition in efficient practice;

- new targets: seeing what others expect and how they measure it. In one instance, an organisation which thought of one process as an overhead, turned its measures into those of a profit centre;

- new ways of working: learning tools and techniques from others. One organisation started using cost/benefit analysis to determine the areas of greatest potential benefit from risk management techniques. The emphasis of risk management was shifted from large risky projects which had full-time project management attention to more mundane operational work activities. Another organisation started to require demanding incident reporting times;

- new roles: changing process objectives and structures by understanding best practice. Many organisations find that benchmarking leads them to adopt new techniques such as genuine profit centre deductions or more formal management systems, e.g. ISO9000.

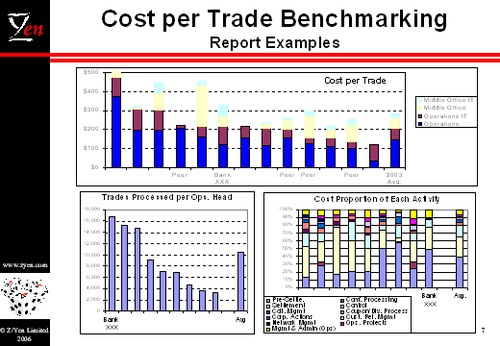

A benchmarking screen might look something like the following examples from the capital markets:

Current ACORD messaging could already provide important benchmarking information, e.g.:

- process times time to write a policy, etc.;

- process outcomes policies written, quotes unused, failures, etc.;

- process efficiency messages per policy written, etc.;

- policy analysis breakdowns of amounts, classes, brokers, etc.

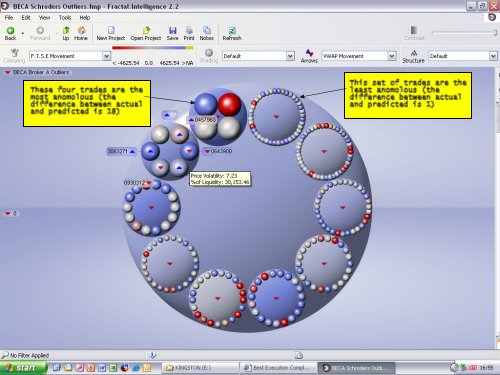

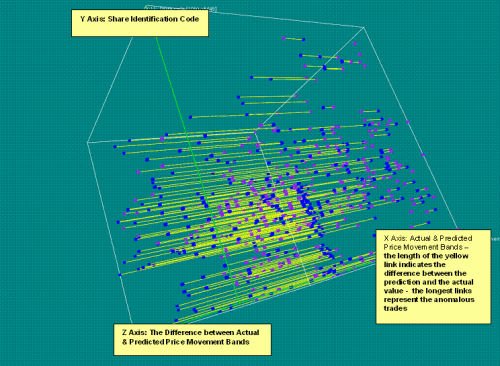

Z/Yen would also like IndeZy to provide pricing and anomaly detectors at data entry points for participating underwriters and brokers on a field-by-field basis using its PropheZy risk/reward software. PropheZy works on an historic data stream to predict what seems sensible, e.g. this policy seems to have been under-priced given what

PropheZy has seen to date. The screen below is a sample of PropheZy detecting anomalous equity trades:

IndeZy the Project

Z/Yen has held discussions with numerous organisations, e.g.:

- Lloyd's;

- ACORD;

- capital markets investment banks, exchanges and index providers;

- capital markets technology companies;

- underwriters;

- brokers;

- insurance markets suppliers IT providers, messaging and hub providers;

- regulators.

Our objective is to see whether a reasonable sample of trades between underwriters and brokers permits us to estimate prices accurately. This would be a statistical study. Similar work in other traded markets has shown that a small sub-set of information can rather accurately predict prices. The IndeZy project seeks information either from a set of underwriters and brokers, or from a messaging information/hub provider, or from a core market organisation.

Next Steps

The most important proof-of-concept is not discussion, but to get a sample of actual insurance policies and prices to see if the information content is rich enough to predict prices.

Z/Yen welcomes discussion on any aspect of IndeZy. For further discussion on any of the above, please contact:

Professor Michael Mainelli

Z/Yen Group Limited

41 Lothbury

London EC2R 7HG

tel: +44 (0) 207-562-9562

email: michael_mainelli@zyen.com