Evidence Of Worth In Not-For-Profit Sector Organisations

By

Ian Harris, Professor Michael Mainelli, Mary O'Callaghan

Published by Journal of Strategic Change, Volume 11, Number 8, John Wiley & Sons, pages 399-410.

[An edited version of this paper appeared as “Evidence of Worth in Not-for-Profit Sector Organisations”, Journal of Strategic Change, Volume 11, Number 8, John Wiley & Sons (December 2002), pages 399-410.]

Abstract

The Not-for-Profit sector is a significant part of the economy. Not-for-Profit sector organisations have a duty to their stakeholders to provide evidence that they are using resources well. The authors have a few decades of Not-for-Profit client work and have conducted some original research amongst leaders of UK Not-for-Profit organisations in order to test their proposition that the Not-for-Profit sector should provide evidence of worth. This research, which is interesting for strategic thinkers in all multi-stakeholder sectors, shows that:

- Not-for-Profits are increasingly aware of the need to provide evidence of worth;

- four themes emerge in demonstrating evidence of worth as Not-for Profits struggle with “internal aspiration versus external imposition”, “outcomes not outputs”, “gathering evidence” and “communication, contribution, consensus, commitment”;

- there are four basic types of Not-for-Profit organisations based on their primary desired outcome, viz. expanding frontiers, changing systems, service delivery and communitarian;

- information to validate evidence of worth may be categorised as risk control, reward enhancement or volatility reduction targets.

For What It's Worth

The Not-for-Profit sector is big business. The John Hopkins Center for Civil Society Studies [Salamon et al, 1999] estimates that the Not-for-Profit sector in 1999 was a $1.1 trillion industry in the 22 countries examined (excluding religious congregations) with 19 million full-time equivalent paid workers. The International Year of Volunteers estimates that a further 10 million people are active volunteers in the sector [www.iyv2001.org]. By way of comparison, a $1.1 trillion industry is roughly the same size as the GDP of the UK. Within each of these 22 countries, the Not-for-Profit sector averages 4.6% of GDP.

Commercial organisations are judged on financial performance, especially if the company is public. Not-for-Profit organisations, especially charities, are stewards of resources that have been provided by and for people and organisations other than the Not-for-Profit organisation itself. The Not-for-Profit organisation has a duty to provide evidence that those resources have been well used. Such evidence is not primarily about financial returns (although financial performance clearly does matter), but more importantly the progress the organisation’s work is making towards its goals (e.g. its charitable objectives).

For over 15 years our people have spent a sizeable proportion of their time working with Not-for-Profit organisations as well as commercial sector organisations. Not-for-Profit people say to us “but you’ve got to understand, we’re different”. Despite the differences, we contend that all organisations should be able to provide evidence that they add value to society.

Comparing Corporate with Not-for-Profit Evidence Models

Not-for-Profits should provide evidence of stakeholder value just as corporates should provide evidence of stakeholder value. This thinking is not new or unique. For example, the UK Charity Commission’s guideline CC60, “The Hallmarks of a Well-run Charity” states that a charity should be “able to show how its activities are, or will be, able to support its charitable aims”. The table below expands on a popular corporate model for shareholder value [Rappaport, 1998] and indicates how Not-for-Profit sector objectives and evidence effectively follow the same principles.

| Level | Corporate Term | Corporate Examples | Not-for-Profit Sector Term | Not-for-Profit Sector Examples |

|---|---|---|---|---|

| 1 | Corporate objectives |

Shareholder returns Shareholder value added |

Charitable objectives (or Organisational goals) |

Relieving poverty in developing nations Saving rare animal species |

| 2 | Valuation components (or Critical Success Factors) |

Positive discounted cash flows Profitability |

Outcomes (or Critical Success Factors) |

Ensuring that households have sufficient able-bodied people Reducing demand for clothing made from rare animal fur |

| 3 | Value drivers (or Key Performance indicators) |

Sales growth Profit margins Capital employed |

Measures (or Key Performance Indicators) |

Reduced percentage of local population contracting HIV/AIDS Number of countries prohibiting rare animal fur |

In this article we shall test the proposition that Not-for-Profits should provide evidence of worth and question the extent to which they do so.

How real are the differences between Not-for-Profits and corporates? Not-for-Profit organisations do tend to have relatively high aspirations but relatively tight resources, often compounded by:

- heavy use of part-time, volunteer people;

- complex influencing behaviours, e.g. lobbying or long-term research;

- third party beneficiaries, i.e. the beneficiaries often have little say in their benefits or little ability to feed back their thoughts;

- tensions between funders’ wishes and charitable objectives, e.g. tied funds for specific work programmes, funds for public relations, corporate funds tied to marketing, government funds tied to political risks.

The aspirations of Not-for-Profits are often a complex portfolio of aims, which generate similarly complex information needs, especially if a Not-for-Profit wishes to provide evidence that it is meeting those aims. This complex portfolio of aims in Not-for-Profits means that they spend a lot of time trying to prioritise and reappraise activities. By prioritising activities, Not-for-Profits start the process of defining benefits and agreeing how their organisations are going to prove they have achieved those benefits. This process is similar to commercial organisations appraising alternative projects for investment. Such an appraisal might not be entirely based on numbers, but it does require definition and demonstrable, measurable benefits. It is especially important for Not-for-Profit organisations to:

- set achievable objectives in their strategies;

- prioritise possible areas of activity and/or projects;

- find “good enough” solutions to maximise the impact of their limited resources;

- record and measure sufficiently to prove that they are meeting the objectives they have set.

Two case studies from our own professional work: The Marine Stewardship Council’s Alaskan Salmon Model and The Children’s Society MART Initiative show how some Not-for-Profits currently provide evidence of worth.

The Marine Stewardship Council’s Alaskan Salmon Model - Case Study 1

The Marine Stewardship Council (MSC)’s objectives are to bring about a sea change in oceans’ management by providing economic incentives for sustainable behaviour and advancing public education in the principles and practice of conservation. The MSC is one of the leading voices in the marine conservation community. It is a global charitable organisation with its international headquarters in London.

The MSC has a refreshingly business-like approach to providing evidence of its worth. Brendan May, the MSC Chief Executive, says “business people are used to undertaking cost/benefit analysis to support their decisions and often feel uneasy when Not-for-Profit organisations advocate solely intangible or qualitative benefits. Of course, some Not-for-Profit issues are intrinsically qualitative, hard to measure and tricky to express in financial value terms. Our argument is that Not-for-Profits should nevertheless try their best to provide empirical evidence to back requests to the business world. This sometimes requires real imagination”.

Z/Yen worked with the MSC to try and prove the tangible value of the MSC's certification scheme for sustainable fishing. Z/Yen used risk/reward option techniques similar to those used by industry to make decisions on large investments; applying the Black-Scholes formula. Using historical data on fish volumes and prices, it was possible to model the Alaskan Salmon industry (five major species of salmon). This model enables the valuation of the reduced market volatility that following the MSC standard should yield (using option pricing theory) and thus is a way to evaluate and measure the scheme’s worth. The Economist reported the findings and conclusions: “the implied saving is more than $1m a year. That is 50 times higher than the cost to the Alaskan Salmon industry of MSC certification - $100,000 every five years” [The Economist, 18 August 2001]. After a few years, the predictions will be replaced with actual data on post-certification volatility. Applying this technique to many species and many fisheries should, in time, provide a substantial body of evidence to support the economic case for demonstrably sustainable fisheries.

This MSC study emerged primarily in order to address external pressure. The MSC executive realised that it needed to provide evidence of the value of the MSC scheme to their stakeholders in order to influence those stakeholders’ behaviour. In the following example, however, The Children’s Society embarked upon its initiative primarily in order to better itself (internal drivers).

The Children’s Society MART Initiative - Case Study 2

The Children’s Society (The Society) is committed to tackling the root causes of problems faced by children and young people, especially those whose circumstances make them particularly vulnerable. It has an annual income of about £40M, runs about 100 social work projects and employs around 1,200 staff.

The Social Work Performance Measurement and Recording Initiative (MART Initiative) was designed to equip social work projects and units with the knowledge and ability to undertake performance measurement and recording in a harmonised way. The benefits sought from MART included encouraging good practice, improving the quality of information, evaluating the effectiveness of practice and providing the ability to measure and learn from information shared between groups of project and units.

The tools designed to support the Initiative were:

- MART: the Measurement and Recording Template, which has been developed by the Society's IT department specifically to support this work. MART is a configurable Microsoft Access database, which provides a common data structure while enabling projects/units to meet local information needs safely, securely & flexibly;

- SMART: Several "MARTs", allowing data from several MART sites to be consolidated for reporting, comparison and shared learning.

The objectives of the Initiative are focussed on skills more than tools. The initiative is based on a sound methodology for analysing and identifying information needs in projects/units. The initial engagement with projects revolves around helping practitioners to think about what they do, what they record and why they do it that way.

The facilitation work is the main resource requirement; two to three full-time equivalent staff over a period of 30 months for the initial roll-out to 120 projects and units. The IT development, on the other hand, was a fairly low-key matter, with one Society Access expert working part time on the initiative for eighteen months or so. In later stages, other Society staff were involved in testing and brainstorming improvements to the tool. Z/Yen was more heavily involved in the early stages, retaining an advisory role in developing improved use of the tool and the methodology. The emphasis from the outset was ensuring that the Society would be self-sufficient once the initiative was implemented

The initiative was primarily intended to help the Society better itself. Nigel Hinks, then Head of Practice Research and Learning at the Children’s Society, said, "the potential benefits go way beyond the recording of data. Those benefits include improved social work practice and the ability to measure and learn from information shared between groups of projects and units, such as programmes of work or geographical groupings. The ‘cyclical’ or iterative methodology is crucial, in my view, to the successful introduction of evaluative approaches in organisations."

Rollout to over 120 projects and units took place between 2000 and 2002. The Society is already using knowledge obtained through this Initiative on other Society Initiatives such as planning and project management of IT projects, information models used for liaison between departments and MART potentially being used as a tool in other Society departments. Prior to the Initiative, many people in the Society, Nigel Hinks included, felt that such an initiative probably “could never happen here”. It did happen, largely because the Initiative was staged (plan, test, review, pilot, review, roll-out, review, refine); an interesting balance between wholesale adoption of the methodology and incremental deployment of the tools and techniques. The Society is now rolling out an agreed set of National Outcomes, requiring each project and unit to measure its performance against those factors to provide evidence of worth.

The Society’s thinking was quite advanced when we began our collaboration in 1998. By sophisticated design, The Society has applied modest budgets very effectively compared with most corporate initiatives of similar size and complexity. Nevertheless, it has committed significant resources to the initiative, including an ongoing team of five for ongoing facilitation and outcome measurement. The Society therefore provides support for our proposition that the Not-for-Profit sector is embracing evidence-based working.

Evidence of Worth Research Programme

The Research

During 2001 and 2002, in order to understand the extent to which the wider community of Not-for-Profits provide evidence of worth, we conducted some primary research designed to test the proposition that “Not-for-Profits are under increasing pressure to demonstrate that they add value”. Our research programme included:

- desk research - where the team attempted to identify best practice around the world, but with an emphasis on the UK;

- client research - where we gathered best practice ideas from the Z/Yen client base, including The Children’s Society and Marine Stewardship Council above, and also included work with The British Red Cross, Cancer Research UK, British Heart Foundation, Barnardo’s and many others;

- structured interviews - where our team met with senior executives of Not-for-Profit organisations;

- seminar and focus groups - a one-day workshop and subsequent break-out sessions;

- synthesis – including circulation of drafts of this paper.

The structured interviews were held with top executives (mostly chief executives, some deputy chief executives and finance directors) in the following organisations:

- The British Council

- Community Service Volunteers (CSV)

- Diabetes UK

- GMB (a large UK trades union)

- Institute of Chartered Accountants in England and Wales (ICAEW)

- Mencap

- National Society for the Prevention of Cruelty to Children

- Oxfam GB

- Royal National Institute for the Blind (RNIB)

- Royal National Institute for Deaf People (RNID)

- St John Ambulance

The structured interviews covered the following topics:

- Organisational Commitment

- Measurement and Monitoring

- Developing Measures

- Forecasting and Targets

- Communication

- Shared Learning

Each topic contained some questions testing our assumptions on Not-for-Profit sector evidence of worth. For example, under measurement and monitoring we asked “are you trying to monitor outcomes and impacts from your work?” and “how did you choose the measures you use?”. Under developing measures we asked “do you try to involve stakeholders (such as service users and beneficiaries, staff, partner agencies, funders) in developing measures?”.

From the structured interviews, we arrived at some preliminary thoughts based around four main themes. In 2002 a seminar was organised and attended by 32 senior people from 24 Not-for-Profit organisations, including several of the interviewees. We introduced the attendees to our findings and themes. We then asked the attendees to work in focus groups to discuss the following questions (which tested our preliminary findings).

| Theme | Question |

|---|---|

| Internal aspiration versus external imposition | What rights do outside parties have to demand evidence of worth? |

| Outcomes not outputs | How can you relate the outcomes you seek to the work you do? |

| Gathering evidence | How do you know when you are spending enough effort on measurement – or not spending enough? |

| 4 C’s – Communication, Contribution, Consensus, Commitment | How do you know when you have enough contribution and can you communicate too much? |

The findings

Internal aspiration versus external imposition – key findings

In several Not-for-Profit organisations, the CEO is the driving force behind evidence of worth initiatives. These CEOs are often “new broom” leaders who are new to their organisations (and often new to the sector) and who bring in new emphases. This finding is consistent with our earlier (cross sector) research into triggers for change, in which we identified direction from the top as one of the key drivers for change [Mainelli, 1992].

Several of these leaders have implemented new governance structures and new types of accountability, to staff, beneficiaries and other stakeholders. In many organisations, the stakeholders have started to demand, impact analysis or evidence of worth. These points are related; as organisations widen their view of stakeholders to include more service users, volunteers and members, those constituencies want to see evidence of worth. “We need to be able to aggregate the feelings – what are our beneficiaries’ own indicators for change; the things we didn’t know we were interested in”, David Nussbaum, Finance Director, Oxfam.

Some leaders bemoaned Government’s lack of a big picture view; Government measures the cost of services but doesn’t seem to measure the benefits arising from charity work. Some wanted more active leadership from the Charity Commission in this area, while recognising that the Commission is at least encouraging moves towards measuring evidence of worth. Many Not-for-Profit leaders welcomed the Government’s Performance Innovation unit raising these issues. Proving value to sustain funding is a key issue for many of the leaders. “In the past too many front line staff believed that a magic bank at the centre would always provide”, James Strachan, Chief Executive, Royal National Institute for Deaf People.

Discussion Group: What rights do outside parties have to demand evidence of worth?

Formal regulators have rights to demand information in much the same way as they do for corporate and public sector bodies. “Survival depends on trust, choice and accountability.” However, there is a risk that pandering to external parties demands can paralyse and/or remove innovation. “We might always go for the lowest common denominator”. There is increasing demand for evidence of worth across all sectors, not just the Not-for-Profit sector. However, the reputation risk from a publicised failure to perform is possibly more sensitive to a charity, which might lose essential public support very rapidly. There surely is a point at which demands go beyond the right to evidence and reach a level of possible obstruction and interference. Finding the appropriate level is difficult as it will vary depending upon the circumstances, such as the objects of various Not-for-Profit organisations. “Management of public expectation is key”.

Conclusion: External demands for evidence should aim to help Not-for-Profit organisations to govern themselves without stifling their opportunities to thrive.

Implication: Not-for-Profit leaders need to encourage bottom-up enthusiasm for monitoring and evaluation.

Outcomes not outputs – key findings

Many participants found it hard to link organisational aims with programme or project specific aims. For example, how do you link the aims of a project to drill and install a village well with an overall objective to reduce the effects of poverty on women. Most participants said that it is much easier to measure activity, or outputs, than to measure the impact or outcomes of their work. Further, many suggested that their funders in Government or foundations only demand output statistics rather than assessment of outcomes, making it harder to promote an evidence-based culture. “It is important to avoid measurement for presentation’s sake”, Patrick Spaven, Head of Research and Evaluation, The British Council.

Some participants suggested that the difficulties in providing outcome information is to some extent a timing issue. “It is a challenge to demonstrate the value of services we have been providing for a long time as opposed to those that have just started”, Fred Heddell, Chief Executive, Mencap. Sometimes the inability to demonstrate evidence of worth can lead to difficult choices, such as discontinuing popular services which might not be providing sufficient benefits to justify the costs and effort. One organisation gave an example of increasing demand for a very effective care helpline, only to learn that the increased output was reducing the quality and therefore the effectiveness of the service.

Discussion Group: How can you relate the outcomes you seek to the work you do?

Some evidence-based assessment needs to rely on “judgement more than measurement”. Over-dependence on qualitative measures tends to be more output focussed and is less likely to be linked to desired outcomes. Z/Yen’s experience seems to support this thinking; for example the Children’s Society MART initiative (see case study above) encourages all projects to build links to desired organisational outcomes to provide evidence of worth. Some Not-for-Profit organisations seem to fear that attempts to assess outcomes will reduce organisational legitimacy, especially if the organisation tries to fudge the answers to provide the messages it wants. “There are risks of not coming up with honest answers.” Those organisations that have implemented evidence-based evaluation suggest that their experience counters this fear.

Conclusion: A Not-for-Profit organisation’s outcome measures should clearly link to its charitable objectives and relate directly to the work done by the organisation.

Implication: Not-for-Profit leaders should have something simple in place, soon.

Gathering evidence – key findings

Several Not-for-Profit organisations are trying to adapt commercial frameworks to the sector, such as balanced scorecards or the EFQM Excellence Model [www.efqm.org]. While some find these frameworks helpful, others reported immense problems adapting and rolling out these frameworks. This accords with earlier research of ours, where we found Not-for-Profit organisations struggling with quality frameworks due to the multiplicity of their stakeholders and objectives [Mainelli and Harris, 1993, 1995]. A common first step was to try to develop measures in national headquarters and then roll them out to local sites. This approach does not seem to work well. “Some front line staff do not want to be fodder for bigger processes”, David Nussbaum, Finance Director, Oxfam GB. Large, centralised initiatives have a tendency to be over-complicated. “Avoid complicated measures that people do not understand”, Patrick Spaven, Head of Research and Evaluation, The British Council.

Devolving a large part of the authority for gathering evidence to operational units seems to work better, although some staff still feel that measurement is being imposed on them even when initiatives are far more “bottom up” than “top down”. Several organisations reported “silos of information”, where staff hold on to information and do not want to pass it up the line. Several organisations suggested a real risk that they might be missing out on changes in demand for services by concentrating on measuring existing work rather than understanding the work in the context of changing or emerging needs. Some organisations observed that there is external pressure to provide immediate evidence, whereas the real evidence of achievement can only be judged in the longer-term, especially where lasting change is part of the objective, as supported by experience of impact assessment of development agencies [Roche, 1999].

Discussion Group: How do you know when you are spending enough effort on measurement – or not spending enough?

The word “spend” in this context was interpreted to mean “some money but mostly time - lots of it”. It is “critical to spend in the right places”. Indicators that suggest that you are spending too little include poor resource allocation, failure to get funding for worthwhile projects and failure to improve through learning. Indicators that might suggest that you are doing enough (or too much) include:

- more accuracy than is needed to provide evidence;

- measurement that is not leading to learning;

- gathering information that neither helps with local decision making nor provides evidence of worth.

Conclusion: Not-for-Profit organisations should treat investment in measurement and organisational learning much like any other investment, requiring a sufficient return for the costs and effort involved.

Implication: Not-for-Profit leaders must emphasise ‘learning from measurement’ as they start to promote evidence of worth initiatives.

4 C’s – Communication, Contribution, Consensus, Commitment

All organisations consistently stated that staff and volunteers/members are the key audiences for communications and that staff commitment was a prerequisite for measuring evidence of worth. “The biggest challenge is internal communications, how to learn and change practice, drive through our partners and then learn back from them”, David Nussbaum, Finance Director, Oxfam GB. Several leaders articulated that challenge in terms of explaining the purpose of initiatives and getting buy-in, especially from staff. “It’s still hard to make the words meaningful to staff”, Chief Executive of a major UK care charity.

Many charities recognise that there is a need to apply resources to these 4C’s – those organisations that have been successful at implementing changes and measuring worth have tended to have dedicated resources, i.e. a person or a unit dedicated to rolling out the initiative to the organisation. However, Not-for-Profit organisations risk local rejection if they are seen to be imposing central methods (see “Gathering Evidence” above). There is a fine balance between being seen to provide resources to help local implementation and being seen to send people to impose central methods.

Several organisations are restructuring their governance, for example initiating councils of members rather than just relying on the board. Some organisations are involving beneficiaries in governance, which can be a difficult exercise in some instances, for example if the beneficiaries have severe disadvantages and/or disabilities. Such structural accountability initiatives are often closely related to evidential accountability initiatives.

Discussion Group: How do you know when you have enough contribution and can you communicate too much?

There is an ongoing need for contribution which needs to be two way. “Give people a voice and feed back to them, otherwise it is seen as a pointless exercise”. A possible (indeed likely) culprit for over-communication is e-mail. Transmitting all messages to all people can become dysfunctional and/or inefficient. “Quality of communication is more important than quantity of communication”. However, in some situations it is good to over-communicate; in particular when building new relationships (e.g. post-merger) or in a change environment where gossip, rumours and fears seem prevalent. “There are times when you more or less cannot over-communicate”.

Conclusion: A Not-for-Profit organisation needs to pay particular attention to communication with and getting contribution from its stakeholder base, but it also needs to avoid the risk of paralysis in doing so.

Implication: Not-for-Profit leaders should repeatedly promote measurement through communication.

As a result of our research, we perceive the sector to consist of organisations that attempt to achieve one or more of the four following types of Not-for-Profit outcomes:

- expanding frontiers to mitigate needs (e.g. a medical charity developing drugs which might cure and/or prevent disease, or a developing world charity adapting irrigation techniques to help meet the needs of farmers in barren places);

- changing systems to remove or release needs (e.g. an advocacy organisation seeking to change government policies which are indirectly leading to abuse of young people in the youth justice system, or an environmental organisation seeking to protect a depleting world resource);

- service delivery to meet needs (e.g. a developing world charity providing care for orphaned children in war-torn places, or a UK charity providing care homes and day care for the elderly);

- communitarian to address needs for or through communal activity (e.g. a volunteering organisation, a trades union or a professional institute).

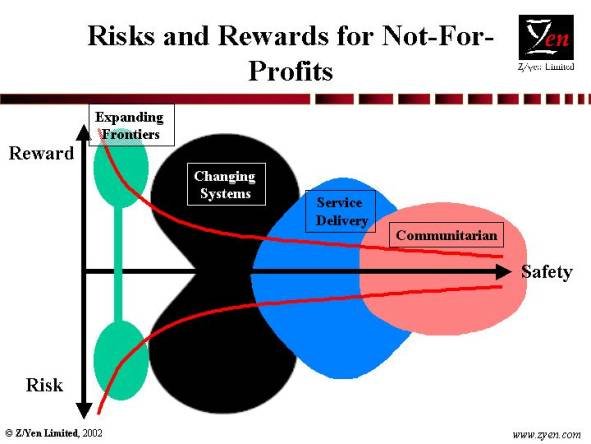

The above categories have different risk reward profiles, and therefore different approaches to meeting information needs and to providing evidence of worth. The following diagram illustrates those differences:

Not-for-Profit activities involved in expanding frontiers, such as finding a cure for a killer disease, will probably achieve outcomes at the high reward or high-risk end of the scale. They either spend lots of money to cure the disease or they spend lots of money but fail. Middling outcomes are unlikely. However, the objectives of such endeavours are usually well defined and it is normally relatively easy to prove and attribute outcomes. Not-for-Profit activities involved in changing systems are also relatively high risk and/or high reward activities. Once again, the objectives are normally well defined and it is usually relatively easy to prove outcomes, although attribution is often problematic. For example, a trades union that claims that its government lobbying and advocacy led to the introduction of the minimum wage is one of many unions and Not-for-Profit organisations that can claim some credit for achieving that objective.

Service delivery Not-for-Profit organisations are undertaking lower risk, lower reward activities than those expanding frontiers and changing systems. However, it can be much harder to define objectives and to prove outcomes arising from service delivery. It is also difficult to define objectives and prove outcomes from communitarian activities. There is also a further complication in communitarian organisations, as volunteers and members are often a mixture of supporters and beneficiaries, with some individuals being both supporters and beneficiaries. Communitarian activities therefore tend to be relatively low risk and low reward.

Many larger Not-for-Profit organisations undertake activities in more than one of the above categories. Indeed some organisations, such as the RNIB, clearly perceive themselves to undertake activities in all four categories (expanding frontiers: research into blindness; changing systems: lobbying for changes in legislation; service delivery: helping the blind; communitarian: promoting a sense of belonging). The appropriate approach to providing evidence of worth and measurement can be substantially different for different activities. This is one reason why attempts by such organisations to take a single, comprehensive approach to evidence and measurement can be difficult. The challenge for a diverse Not-for-Profit organisation is to understand its portfolio of activities and to establish appropriate, diverse measures and means to provide evidence of worth.

The four categories of Not-for-Profit activity set out above arose through the original research documented in this paper. However, when we embarked upon this study we had already identified commercial use of three categories of information based on three types of risk/reward governance.

- avoiding or managing risk;

- reward enhancement;

- reducing volatility or assuring quality of life.

We tested these information categories in the Not-for-Profit sector, and found that they seemed to apply. The following table contrasts the three types of information that Not-for-Profit sector organisations can use to provide evidence of worth against each category of activity.

| Three types of information | Expanding Frontiers | Changing Systems | Service Delivery | Communitarian |

|---|---|---|---|---|

| Risk Avoidance/ Management | minimising direct and indirect cost of failures | reputation maintenance | minimising adverse incidents | minimising volunteers’/ members’ issues and concerns |

| Reward Enhancement | commercial value directly or indirectly caused | impact of changes on communities | achieving outcome targets | maximising rewards to volunteers/ members |

| Quality of life/ Volatility Reduction | consistency of progress in line with targets | value of reduced volatility and/or improved quality arising from changes | maintenance of service standards | volunteers’/ members’ satisfaction with representation provided |

We suggest that, as a minimum, a Not-for-Profit organisation should have at least one objective in each of the categories of activity it undertakes for each type of information, i.e. three objectives per activity. Each objective may well have subsidiary success factors, for instance the “reputation maintenance” example above (risk avoidance/management: changing systems) might well have subsidiary factors for perceived political lobbying clout, consumer brand awareness or affinity for the relevant community. A charity such as the RNIB, which undertakes all four categories of activity, might structure 12 overall objectives with subsidiary success factors.

Where Next For Evidence Of Worth?

The ideas suggested in this journal paper need further testing by Not-for-Profit organisations. We hope that the wider circulation of these ideas will generate further discussion and testing. We see the link between evidential accountability (evidence of worth) and structural accountability (governance) to be a key trend for the Not-for-Profit sector, as indeed it is proving to be in the commercial sector. Further research will focus on how Not-for-Profit sector approaches to governance link with evidence of worth.

References

- Lester M Salamon, Helmut K Anheier, Regina List et al, Global Civil Society: Dimensions of the Nonprofit Sector, Johns Hopkins Center for Civil Society Studies, Baltimore, 1999.

- Alfred Rappaport, Creating Shareholder Value, The Free Press, 1998.

- The Economist, “A Novel Use for Options Theory – Fishy Maths”, 18 August 2001, page .

- Michael Mainelli, "Vision into Action: A Study of Corporate Culture", Journal of Strategic Change, Vol 1, pages 189-201, John Wiley & Sons, 1992.

- Michael Mainelli and Ian Harris, "Quality Management in Charities", The Charities Finance Handbook, 1995.

- Michael Mainelli and Ian Harris, "Reaping the Rewards of Quality", NGO Finance, Volume 3, Issue 2, pages 22-24, June 1993.

- Chris Roche, Impact Assessment for Development Agencies, Oxfam Publishing, 1999

The authors would like to thank Nigel Hinks of The Children’s Society for his contribution to The Children’s Society case study; Brendan May of the Marine Stewardship Council for his contribution to the MSC case study; and HSBC Charity Fund Managers for facilities provided to aid the research.

Ian Harris leads Z/Yen’s Not-for-Profit sector practice. Ian specialises in strategic planning, systems design, rewards planning and organisational change. Not-for-Profit sector clients include Barnardo's, Cancer Research UK, Women’s Royal Voluntary Service, BEN, Macmillan Cancer Relief, British Heart Foundation, The Shaftesbury Society, UNISON and The British Red Cross. Ian is also a regular contributor of articles and pieces for the business and Not-for-Profit press. He is co-author, together with Michael Mainelli, of the recent, practical book "IT for the Not-for-Profit Sector" and their best-selling humorous management novel "Clean Business Cuisine". Michael Mainelli is Z/Yen’s Chairman working across a variety of sectors (banking, insurance, media, utilities, television and distribution as well as Not-for-Profit organisations) on problems ranging from strategy through information systems, quality, human resources and performance improvement. Michael is a former Vice-Chairman of The Strategic Planning Society (a registered charity), a member of the Advisory Board for City University’s School of Informatics and a trustee of the Ocean Alliance/Whale Conservation Institute. Michael was a partner in a large international accountancy practice for seven years before a spell as Corporate Development Director of Europe’s largest R&D organisation, the UK’s Defence Evaluation and Research Agency, and becoming a director of Z/Yen in 1995. Mary O'Callaghan is a senior Z/Yen consultant with a background in business research and development. Her recent work for Z/Yen has included planning, implementation and evaluation of performance measurement, recording and review systems for The British Heart Foundation, Cancer Research UK, The British Red Cross and The Children's Society. Prior to Z/Yen, Mary was a conference director for one of the leading UK conference organisations. Prior to that, Mary worked in the Not-for-Profit sector, specifically in arts administration. Z/Yen Limited is a risk/reward management firm working to improve organisational performance through successful management of risks and enhancement of rewards. Z/Yen undertakes strategy, systems, people, intelligence and organisational change projects in a wide variety of fields.