Why Bother To Be Better? Strategically Stagnant Personal Current Accounts

By

Stephen Martin, Professor Michael Mainelli

Published by Journal of Strategic Change, Volume 12, Number 4, John Wiley & Sons (June-July 2003), pages 209-221.

Strategically Stagnant Personal Current Accounts

Banks are keen to supply current accounts because apart from direct income, they are more successful in selling a wide range of their financial services to customers who possess a current account. The UK market for current accounts appears to exhibit little customer movement and is dominated by 4 out of at least 140 suppliers, despite variable levels of service. Using prospect theory, attempts are made to explain why this market is so stagnant and to suggest how suppliers could be more successful at promoting change. Results suggest that changing the initial perceptions of customers will have more impact than trying to induce customers to change suppliers by promoting the benefits of an alternative bank.

The UK Banking Market for Personal Current Accounts

In the UK there are 385 banks registered with the British Banker's Association, 184 of these are incorporated within the UK . Not all of these banks offer a personal current account (PCA) that is equivalent to the "checking account" in the US, but there are 140 different PCAs available in the UK, with the larger banks offering several different types. The suppliers who do provide a PCA can be divided as follows:

- Big Four: Barclays, Lloyds TSB, HSBC, NatWest(Royal Bank of Scotland)

- Other Major Banks: Bank of Scotland(BoS), National Allied Bank(NAB), Abbey National, Alliance & Leicester, Halifax, Nationwide

- Minor Banks: All other banks who offer a PCA in the UK

A Stagnant Market

There is a glib comment that, in the UK, people change their husband or wife approximately twice as often as they change their bank account. This comment is supported by contrasting the market share of the leading banks in the UK PCA market with the UK divorce rate (approximately 40%). The only significant change in share over the last 6 years has resulted from the acquisition of one bank by another.

Figure 1 - Market Shares of PCAs of Leading UK Banks 1995-2000

| 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | |

| Barclays | 17% | 17% | 17% | 17% | 17% | 18% |

| HSBC | 13% | 13% | 13% | 14% | 14% | 14% |

| Lloyds TSB | 24% | 24% | 24% | 24% | 23% | 22% |

| NatWest (RBS) | 18% | 17% | 16% | 16% | 15% | 18% |

| RBS | 4% | 4% | 4% | 4% | 4% | 18% |

| BoS | 2 | 2 | 2 | 2 | 2 | 2 |

| NAB | 5 | 5 | 4 | 4 | 4 | 4 |

| Abbey National | 4 | 4 | 5 | 5 | 5 | 5 |

| A&L | 3 | 3 | 4 | 3 | 4 | 3 |

| Halifax | 3 | 3 | 4 | 5 | 5 | 5 |

| Nationwide | 2 | 2 | 2 | 2 | 2 | 3 |

| Others | 6 | 6 | 6 | 5 | 6 | 6 |

Source: Financial Research Services (FRS)

Note: *Barclays 2000 figure includes acquired Halifax accounts

**Natwest acquired by RBS in 2000

The PCA market share seems ‘stagnant’ and ‘stagnant’ markets are not normally competitive. Where there are a large number of customers and a significant number of competing suppliers then a ‘stagnant’ market could be seen as positively abnormal.

Figure 2 - PCA Ownership in the UK

| Ratio | ||

| ‘Stock’ of PCAs | 46,299,000 | |

| UK adult population (>15) | 47,897,000 | 0.97/person |

| UK households | 24,290,000 | 1.91/household |

(Source: FRS Data, 2000)

Almost every adult in the UK has a PCA. According to a survey for the Director General of Fair Trading (DGFT), 86% of households have a least one PCA at the time of the research. It is increasingly difficult for consumers to do without the facilities offered by a PCA. Crucial consumer suppliers, such as domestic utilities, actively encourage and incentivise payment by direct debit, which is only possible with a PCA.

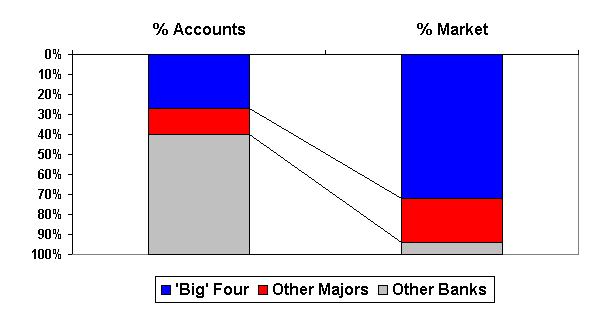

Competing for these customers are, at least, 140 different types of PCA . At first glance this number of alternative PCA choices should generate a highly unconsolidated market. However, the 'big four' banks hold a disproportionate share of the market even when all of their different types of PCA are considered. Whilst the aggregate share of the 140 available accounts that the 'big four' hold is only 27%, these holders of these accounts represent 72% of the market.

Figure 3 - Banks in the UK

Given the amount of competitive marketing in the financial services sector and the changes implicit, as banking goes on-line, is this stagnation a strategic choice or the passive outcome of bank and customer behaviour?

Personal Current Accounts (PCAs) are important to the banks

Banks have found that PCAs are a 'gateway' to selling other financial products. According to Lloyds TSB "the PCA remains the key relationship product" . Abbey National states that a PCA provides almost 100 customer contacts a year, much more than other financial products.

Evidence from Lloyds TSB is that customers who hold a PCA are two to four times more likely to hold another Lloyds TSB financial product. The table below indicates that Lloyds TSB has a higher market share within their own PCA customers than they have within the market as a whole. Whilst this does suggest a general pattern of cross holding of financial products, it does not mean that the cross selling has been from PCAs to other products rather than vice versa.

Figure 4 - Cross-holding of financial products by Lloyds TSB PCA customers, December 2000

| Average number of products | Number of Lloyds TSB products | Lloyds TSB market share of customers | Lloyds TSB market share of market | |

| Mortgages | 0.4 | 0.1 | 25% | 9% |

| Credit cards | 1.1 | 0.3 | 27% | 14% |

| Loans | 0.3 | 0.1 | 33% | 12% |

| Savings | 0.9 | 0.3 | 33% | 10% |

| Household insurance | 0.8 | 0.2 | 25% | 6% |

| Life assurance | 0.7 | 0.1 | 14% | 4% |

| Personal investments | 0.5 | 0.1 | 20% | 5% |

| Personal pensions | 0.1 | 0.0 | 0% | 6% |

| Total | 4.8 | 1.2 |

(Source: Competition Commission calculations based upon FRS data, 2001)

Regardless of the causality of financial product purchase, the PCA seems to represent a pivotal financial product that provides:

- a direct opportunity for profit;

- potential opportunities to cross-sell additional profitable financial products;

- an important opportunity for a high level of customer contact.

It might be assumed that the PCA is a financial product where banks aggressively seek to defend current customers and acquire new customers.

Switching Suppliers in the Personal Current Account Market

However desirable PCA holders may be to various banks, there seems to be little customer appetite to change suppliers. Banks who provide PCAs appear to operate in a market where the 'rewards' for being a better bank are hard to perceive. The following table indicates that, contrasted with mortgages and home insurance, PCA customers rarely switch or consider switching accounts - energy purchase is included as a non-financial comparison:

Figure 5 - Results from DTI Survey: Switching Suppliers

| % in last 5 years that have: | PCAs | Mortgages | Home Insurance | Energy |

|---|---|---|---|---|

| Switched | 6 | 12 | 30 | 32 |

| Considered switching | 15 | 32 | 23 | 14 |

| Neither switched nor considered switching | 76 | 56 | 47 | 54 |

(Source: DTI, 2000)

The Impact of Advertising

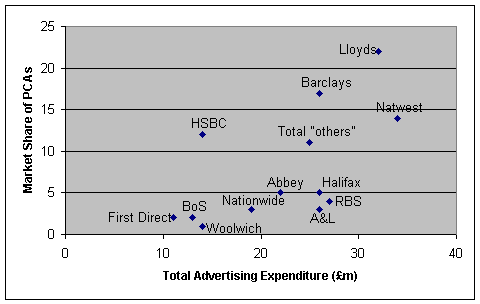

If customers don't appear to change PCAs easily, this is despite high levels of marketing expenditure within the financial services sector and switching in related mortgage and home insurance products. Banks spent £313m on advertising in 2000. The graph below shows that while there is a tentative relationship between total advertising expenditure and PCA market share, there are significant exceptions to the trend and virtually no relationship at lower market shares.

Figure 6 - Graph of Bank Advertising Expenditure versus Bank Market Share

(Source: UK Competition Commission Report quoting Abbey National data, 2001)

Theoretically, if marketing and market share are related, there may be a relationship between the change in market share and the marketing expenditure. However, even within the 'big four' this is clearly not true. Barclays and HSBC have both increased their market share by 1% in the five years to 2000, despite very different levels of marketing investment. Lloyds TSB have dropped by 2% despite spending more than Barclays or HSBC and NatWest/RBS could be said to have jointly declined by 4% despite having a joint expenditure of more than twice as much as Barclays.

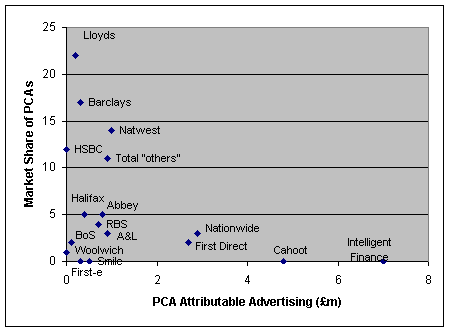

The relationship between market share and expenditure, feeble as it is, disintegrates completely (perhaps even becomes negative) when some effort is made to relate PCA market share to the £23.5M that was spent on advertising that is directly attributable to PCAs:

Figure 7 - Graph of Bank PCA Specific Advertising versus Bank Market Share

(Source: UK Competition Commission Report quoting Abbey National data, 2001)

Much of the higher expenditure is by banks that are growing their brand awareness. Again there is no connection between the 5 year growth in market share and the current level of expenditure. This poor correlation might be partially explained if much of the marketing related to PCAs is unmonitored advertising expenditure, (e.g. direct mail) which would be excluded from the figures represented in Figure 5. It is also possible that the aggregate expenditure of the last 5 years may be related to the aggregate growth (or decline) in market share. However given that the largest cost in most consumer focussed marketing is advertising and given that there has been very little net movement in market share it is more likely that there is little or no relationship between expenditure and market share.

Other Drivers for PCA Supplier Choice

If increasing awareness through advertising does not have an impact, perhaps satisfying other customer needs determines PCA market share. FRS data indicates a range of customer priorities for opening a PCA:

Figure 8 - Reasons for Opening a Specific PCA

| % | |

| Convenient branch location | 27 |

| A contact holds account or works there | 18 |

| Recommended | 18 |

| Already have other products there | 12 |

| Reputation/image | 8 |

| Availability of ATM | 6 |

| Services available | 6 |

| Attractive overdraft package | 5 |

| Attractive interest on credit | 5 |

| Offers direct banking | 5 |

| Incentives | 3 |

| Advice | 3 |

| Lower charges | 3 |

| Opening hours | 3 |

| Range of products | 2 |

| Ethical stance | 1 |

(Source: FRS Surveys 2000)

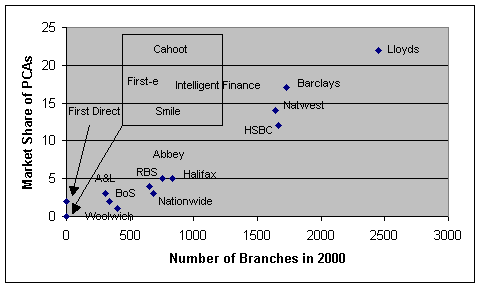

This table suggests that customers give greater weight to the branch location and whether they know someone who uses or recommends the bank. Reputation (somewhat related to brand and advertising), the nature of the services and level of the charges (or incentives) play a much lower level of importance in the selection process. The importance of convenient branch location is supported by the following graph indicating a strong relationship between the number of branches and the market share of PCAs.

Figure 9 - Bank Branch Numbers versus PCA Market Share

(Source: Competition Commission, 2001)

This graph suggests the number of branches could explain the market share. This suggestion is not encouraging for telephone or e-banks supplying services without a branch network. However, branch numbers may be reversing cause and effects, i.e. banks have more branches because they formerly had more market share in the 'bricks and mortar' age.

Customer 'Loyalty'

In Figure 8 above, 'convenient branch location' is the most important factor, this is not a very sophisticated supplier selection criteria. Service, recommendation, 'added value' and the range of financial products are all less important to the customer than the location of the branch. This implies that a new PCA is purchased in much the same way as a tank of petrol - a combination of need and location. However unlike petrol purchasers, PCA customers remain incredibly loyal to their supplier. Every year there is some movement in the 'stock' of PCAs, but the rate of growth and change is very small when compared to the overall stock.

Figure 10 - Estimated Rate of Switching and Annual Growth Rate of PCAs, UK 2000

| PCA Movement | Numbers | % |

|---|---|---|

| ‘Stock’ of PCAs | 46,299,000 | 100 |

| New primary PCAs | 661,000 | 1.4 |

| New secondary PCAs | 678,000 | 1.5 |

| Other new PCAs | 635,000 | 1.4 |

| Net new PCAs | 1,974,000 | 4.2 |

| Closed PCAs | (1,321,000) | -2.9 |

| Switched PCAs | (594,000) | -1.3 |

| Net real growth in PCAs | 59,000 | 0.13 |

(Source: FRS Data, 2000)

This data could be misleading about true 'loyalty' as it only shows changes in account ownership and not changes in account behaviour. For instance a customer may increase usage of an alternative or secondary PCA and reduce usage of the assumed primary PCA. From an external analytical perspective, it is next to impossible to know the degree of account usage by PCA provider. Actual percentage levels of growth and change in accounts might be much higher if dormant accounts were defined and excluded from the calculations. Over the period 1997 to 2000 the Consumers' Association has estimated that on average, only 23% of new PCAs represented a switch from an alternative provider indicating that approximately 152,000 accounts (0.33%) change hands annually.

The Cruickshank report in 2000 indicated that banks made the most money on low transaction accounts that had high average positive balance. Accounts in credit in the UK in 1998 had an average balance of £1,175 and generated up to £75 in income . It is therefore possible that banks may not want to highlight dormant accounts or increase account activity within active ones.

Barriers to Switching Suppliers

It is possible that the loyalty shown to PCA suppliers relates to barriers to switching in the market. The Competition Commission identified the barriers to switching PCAs, in their 2001 report on the proposed merger between Lloyds TSB and Abbey National as:

- consumer fears regarding their credit status - con sumers may see advantage in having a long term banking relationship when seeking credit;

- consumer fears regarding disruption to other financial relationships that may be linked to the PCA;

- delays and costs associated with switching accounts, in particular regarding transfer of direct debits and other automated transactions to the new account.

However the Cruickshank Report also refuted these consumer fears noting that:

- wide availability of consumer credit and the sophistication of current credit scoring techniques means that personal customers are highly unlikely to lose credit status if they switch PCA supplier;

- only 14% of PCA customers who had switched had experienced any problems and financial service providers are continually improving their 'switching' resources so t his percentage should decline;

- switching has been lengthy in the past (taking up to six weeks) but that Lloyds TSB (at least) had made a commitment to provide the PCA information to the new supplier within 3 days.

These barriers to switching seem to be more perceived than real; more 'excuses' than real barriers to change. However 'Loyalty' or 'Apathy' or 'Inertia' is so strong that the consumer magazine Which? has launched the 'Switch with Which?' campaign to encourage customers to change banks. The core theme of the campaign is to encourage people who hold a PCA with one of the biggest four banks to switch to a supplier who offers competitive rates of interest on their PCAs. Which? estimates that if the 70% of people who bank with the 'big four' banks switched to one of the best alternative accounts consumers could save up to £500M in total. Given that the biggest four banks represent 72.1% of the PCA accounts, the Which? figures suggest that approximately 50% of PCA customers are using a poorer PCA product than they could be.

Whether customers are seeking better rates, more flexibility or better service, the benefits of switching are real. This 'loyalty' to suppliers of obviously inferior financial products is difficult to explain.

Triggers for change

So, the key question for banks wishing to grow their market share of PCAs (and especially banks without branches) is, what triggers a switch in PCA supplier and what causes resistance to switching? The reasons given for switching PCAs are:

Figure 11 - Reasons for switching PCA

| % | |

| Staff attitude | 20 |

| Better account | 18 |

| Account charges too high | 18 |

| Transaction errors | 17 |

| Poor advice | 8 |

| Not enough branches | 7 |

| Incorrect charges | 7 |

| Refused overdraft | 3 |

| Refused other product | 2 |

| Do not need account | 7 |

(Source: FRS surveys 1998, 1999 & 2000)

The reasons given in Figure 11 can be categorised as follows:

- 59% Negative (staff attitude, transaction errors, poor advice or incorrect charges, insufficient branches);

- 18% Policy/Infrastructure (account charges);

- 18% Positive (attracted by a better supplier account);

- 7% Need (no need for the account);

- 5% Credit rating refused

It appears that in the UK PCA market there is little net growth and low levels of supplier change. Where change occurs, it is usually for negative reasons. Positive change prompted by the offer of a better PCA only drives 18% of the change in the market. This implies that avoiding poor service delivers more customer retention benefit to banks than seeking to improve service related to PCAs. Additionally being better only matters if a purchase comparison is being made. The Cruickshank report suggested that 60% of new PCA buyers in the last 5 years only considered one provider. New account holders, at least, are not making a comparative choice as they buy a PCA.

Any temptation to change supplier is likely to be constrained, as the top three factors considered when choosing a bank are, location (27%), a contact at the bank (18%) or a recommendation (18%). This means that even if a customer is determined to change they are likely to consider the limited alternative bank with the most convenient location with which they either have some contact or some positive recommendation. Banks therefore are not under pressure to be better than other banks, from a customer point of view, a bank can appear to be no worse and therefore change is not worth the effort required. However if the number of branches continues to reduce then banks will increasingly have to try and improve their reputation so that this positively impacts customers' choices.

Pursuit of Perfection

Business should be a competition between the best and the rest, but on the basis of the evidence presented so far, banks seem different. Most pundits advise businesses to pursue competitive strategies that develop and sell a point of difference that is valued by the customer. Business slogans emphasise focus and difference - "stick to the knitting", "unique selling point". Mathur and Kenyon say that "the task of business strategy is to make the business more valuable by a specific route: that of targeting profitable customers" . Over time this difference is supposed to develop into competitive advantage and eventually translate into greater comparative profit.

Underpinning the pursuit of excellence is the assumption that customers will tend to choose the best product or service based on price, convenience or functionality. It is further assumed that customers will change supplier or product or service when offered something better. Even allowing for inertia, this process should at least occur over the long term such that the best should displace the mediocre and the worst.

But customer inertia is a real and significant problem. Although a move to the best should occur (despite Keynes' pointed observation about the long term ), more pressing problems arise in the short term. First, being better generally costs more money than being average. Second, there is no use being better unless this quality is noticed, and 'getting noticed' costs. Thirdly, there needs to be a 'reward' for being better, whether in increased margin, increased customer retention or increased customer acquisition relative to the competition. Without a reward for being better, higher costs will reduce comparable profit.

The stability in the market shares of PCAs could imply that the process of changing banks is triggered more by a 'state of mind' than by an objective comparison of relative value. The DTI 2000 figures in Figure 5 above suggest that only 21% of the PCA customers are unstable enough to switch or consider switching their PCA, whereas more than twice as many mortgage customers (44%) and home insurance customers (53%) are unstable enough to change or consider changing. It would be interesting to understand how something as intangible as 'state of mind' could predictably explain the customer behaviour in the PCA market.

Prospect Theory

There is an arm of decision-making theory that may explain the behaviour in the PCA market. Prospect Theory attempts to describe why individuals make decisions that deviate from rational decision-making. Rational decision-making is a model that assumes decision-makers define the problem; identify and weigh criteria according to their preferences; know and assess all relevant alternatives; and accurately calculate and choose the alternative with the highest perceived value. Economists, and other social scientists with an interest in decision-making, have found that the difference between the rational model (how decisions ought to be made) and the real world (what decisions are made) is so significant that their rational models can be of little use. Increasingly, economists are trying to take into account empirical work on decision-making in the real world. Prospect Theory attempts to explain why some types of real world decisions deviate consistently from rational decisions.

Prospect Theory was first put forward by the Nobel Prize winner Kahneman with his colleague Tversky in 1979. In short, Prospect Theory recognises that people treat risks concerning perceived losses differently from risks concerning perceived gains. Prospect Theory therefore emphasises the importance of framing the choice to the consumer. The way, in which a choice is presented, i.e. as starting from a position of gain or from a position of loss, is crucial to the subsequent behaviour of the consumer. The difference between Prospect Theory and economic theories of diminishing marginal utility is that marginal utility assumes that people only consider their choices in terms of the final outcome, not from where they start, i.e. their 'state of mind' at the start of a decision making process.

Prospect Theory suggests that if you want to drive consumers towards a risk-seeking (dangerous) choice, convince them that they are already losing. If you want to drive consumers towards a risk-averse (safe) choice, convince them that they are ahead and stand to lose. Driving consumers towards risk uses a phrase such as "you have to speculate to accumulate", whilst to drive them away from risk uses, "let's not throw good money after bad". Both phrases take advantage of framing to move the consumer's perspective. To speculate implies you are already behind. To throw good money implies they are in a position where they stand to lose more.

Prospect Theory indicates that the lack of supplier change in the PCA market results from a customer perception that the status quo is not bad enough to drive customers to consider the risk of change. Prospect Theory therefore suggests that successful marketing needs to address (and undermine) the comfort inherent in the current situation rather than focussing upon the benefits resulting from any change. The theory would also suggest that customers would act irrationally to preserve the status quo until they really believe that they are currently losing. Change only occurs when the status quo is really believed to be worse than the alternative of change.

How Banks Should Respond to Prospect Theory

How banks should respond is guided by whether they are seeking to defend the status quo or to promote change of PCA supplier. This creates two broad groups of competing banks.

Defend status quo (72% of the market):

- Branch led side of the 'big four' (Barclays, HSBC, Lloyds TSB, RBS/NatWest)

Promote customers to change or consider change (28% of the market):

- Non 'big four' banks and the non branch sides of 'big four'. (e.g. internet, telephone bank)

Defend the Status Quo

If the primary objective is to support the status quo ('big four' 'branch led' PCA supplier) then the customers need to be encouraged to feel good (or at least no worse off) if they choose to stay with their current supplier. As this position represent 72.1% of the total market then this 'tone' will be very dominant in the market. Bank advertising will tend to emphasise longevity, size, competence and tend to dwell little on detail. There will be relatively little focus upon attracting new customers (compared to reassuring existing ones), as any general move towards changing supplier is likely to be as risky for the bank as it is rewarding.

Change the Status Quo

If the primary objective is to undermine the status quo (anybody but the 'big four' traditional banks) then the focus of the activity should not be to promote the ease of change, but rather to increase dissatisfaction with the incumbent supplier.

The main marketing problem that needs to be overcome here is not a fear of change but a motivation for change. Customers need to be encouraged to feel that existing stability in the market is working to their disadvantage. Bank advertising should identify the cost of stability in much the same way as Direct Line identifies the cost of purchasing home insurance from the mortgage supplier.

Creating an atmosphere for change could present further problems where the PCA supplier that wishes to encourage change is a business unit within a bank that benefits from the status quo. This problem is the one that faces the Internet and telephone banking arms of the 'big four' banks.

However for a smaller supplier seeking to attract customers away from the 'big four' there is a risk in simply promoting change. The primary driver for selecting a PCA supplier seems to be the location of the branch. This raises the risk that a destabilised customer seeking to change PCA supplier will simply settle on the supplier whose branch is closest or most convenient. This would reduce much of the value of the bank's marketing and present a huge problem for banks that offer a branchless proposition.

If customers are to move they need to be destabilised and educated rather than just enticed and attracted.

Recommendations

Clearly the recommendations for action depend upon the starting position.

- Traditional Branch Based Bank ('big four');

- Emphasise stability and heritage (and longevity of account holding);

- Encourage cross selling of financial products;

- Emphasise local contact through the branch;

- De-emphasise savings (as current account returns are low);

- De-emphasise standing orders and direct debits (as activity reduces profitability);

- De-emphasise comparison with other banks (encourages action).

Non-traditional Branchless Banking

- Identify strong reasons for not staying with the same bank for a long time;

- Emphasise that banks are different;

- Identify that branches are not necessary for good service;

- Emphasise interest rates and personal service;

- Emphasise that changing is easy and low risk;

- Encourage setting up a savings account to 'try out' alternative banks.

The 'branchless arms' of the 'big four' have the most complicated communication task. They need to promote change without disrupting the status quo. This suggests that they will need to understand the complex and specific reasons why PCA holders would be willing to change their banking behaviour and yet stay with one of the 'big four' banks who (objectively) may have a financially uncompetitive PCA product.

Current 'State of Mind' of the PCA Customer

'State of mind' depends upon whether one is trying to defend against change or promote it. For customers of the 'big four' customers) the primary objective is to justify the status quo. They are probably aware (at least in part) that there may be better suppliers, but they would like to reassure themselves that the rewards of change are balanced or completely eliminated by the risks of change. These individuals are strong supporters of the belief that banks are equally bad, because this simplifies their life and provides endorsement for their lack of action. Curiously enough, in this environment there is no shame in having a bad supplier (as it is a common problem) and there is a 'comforting misery' in sharing horror stories about banks that often end with the epithet that "all the banks are as bad as each other".

Unless a customer perceives that the status quo is actively detrimental and that change is both rewarding and possible then the status quo will persist. It is not enough to simply sell the benefits of change; it is also necessary to undermine the benefits of the status quo.

Current Banking Communications

When contemporary bank behaviour is profiled against these recommendations the logic of differences between the communications becomes apparent. In some cases it appears that the banks are not trying to increase PCA market share.

| Bank | Campaign | Key Messages | Prospect Theory Interpretation |

|---|---|---|---|

| Lloyds TSB | Your Life. Your Bank | Cross selling of financial products, the heritage of the bank and its services for small businesses | Broadly risk-averse as it implies benefits of large established bank |

| NatWest | Another Way | Traditional branch based banking, service and convenience are key themes. | Risk-averse |

| Barclays | Fluent in Finance | Finance experts, (previous campaigns emphasised size and Internet services) | Currently neutral for PCA promotion |

| HSBC | The World’s Local Bank | Emphasising their global capability and strength | Neutral for PCA promotion |

| Abbey National | Because Life’s Complicated Enough | One stop financial service supplier | Risk-averse but not one of the ‘big four’! |

| Halifax | Giving You Extra | 30x as much interest as ‘big four’ PCA | Risk-seeking but rates are not seen as a key factor (5%) |

An overview of current communications of the largest banks would seem to indicate that HSBC and Barclays are targeting large business customers, whilst Lloyds TSB is considering small customers and PCA holders. NatWest and The Abbey National are the only banks emphasising traditional branch-based banking and thus the status quo. But only NatWest is likely to benefit from this, as it is one of the 'big four', The Abbey National is unlikely to encourage change, but is promoting the traditional model of banking. Cahoot, the bank that has one of the highest levels of PCA attributable advertising, seems to take the line that their unknown brand has financial cachet in their "He's got Cahoot" TV advertising. This approach by Cahoot is unlikely to be believable or motivating to PCA customers and may account for their lack of market share growth.

Most of the other suppliers are promoting the better service, interest rate, account policies and flexibility of their accounts. Although this will attract some customers from traditional banks it is only likely to impact 1 in 6 (18%) of the opportunity customers. The majority of reasons that people give for changing bank (see Figure 11) are negative and until their current PCA supplier is seen in a negative light, large scale change will not occur. Even if the focus was to attract individuals who, as yet, have no PCA then range of services and the interest rate are minor attraction factors with less than 10% significance (see Figure 8).

In addition to its advertising campaign, Lloyds TSB have just announced (January 2003) that they will pay 3.2% interest on their PCA, a move that is likely to cost the bank between £50m and £100m. As they have been losing market share at a rate of approximately 0.4% per year for the last few years the bank must hope that this cost will reduce the loss of, approximately, 180,000 accounts annually. Prospect Theory and the customer research would suggest that Lloyds TSB is 'pulling the wrong lever' if it wishes to effect change in the UK PCA market.

Prospect Theory suggests that if a bank really wishes to create change, they have to start by 'framing' the current situation negatively. Selling the benefits of change and addressing the risks of change have to come after the customer has begun to see their current situation as unacceptable. If customers can be persuaded to take another look at their current bank and begin to see that the longer they stay the more they lose then change becomes more likely. Activity that frames the current customers as losers is the necessary first step for them to accept the 'cost of change'. Potential ways of 'framing' a positive or negative status quo could be:

| Support the status quo | Undermine the status quo |

|---|---|

| Banking is about people not systems, come to our branches and get help with …….. | 33% of a bank’s costs (unknown) pay for the branches, but most people only visit the branch once a year. Why are you paying for a service you don’t use? |

| In this modern world you need to be connected to a connected bank. We can provide everything you need and a local friendly face in your branch. | Internet and telephone banking is cheaper so you get better service and cheaper financial services if your bank is not paying for branches |

| Finance is risky, you should use a bank that has been doing it for a long time and that is connected to your community. | People in the know, bank with us. 85% of our customers have had a bad experience with a traditional bank and moved to us. Why don’t you move when you are unhappy? |

Interestingly a very similar contest between upstarts and established suppliers is currently taking place in the airline industry. The main difference is that it is the established players that are fighting for the consumer attention which has been drawn to the price cutting 'upstart' budget airlines.

The established 'big four' banks could be finding that promoting clearly competitive messages is difficult. Much of the activity in the PCA market derives from one of the 'big four' banks who have most to lose if there was a culture of change in the PCA market. Whilst all of these banks have branchless banking arms that wish to grow, this growth will often be at the expense of the traditional business. The dissonance between the positive messages (reinforce the status quo) of the 'branch side' of the bank would be at odds with the negative framing of traditional branch based banking. It is possible that the marketing departments would therefore tend to focus upon the positive messages of branchless banking rather than then negative framing of traditional banking, even though this is likely to be much less productive and represent a waste of marketing budget. In other words, a negative message that could encourage change is being buried.

Champion for Change

Which? issued a press release commenting upon the UK PCA market where they quote research on customer satisfaction and an increasing tendency to switch supplier.

However change on a major scale is unlikely to happen until a 'critical mass' of organisations are willing to question the model of traditional banking and to spend enough money to change national perceptions. Which? may represent such an organisation, but it is unlikely that they will effect a national change in attitude unless their cause is adopted by many other organisations.

Why Bother to Be Better?

The momentum for improvement is created by a desire for better services on the part of the customer and a desire for an increased number of better customers on the part of the service provider. A change of supplier will only occur when the customer believes they will be better off after the change.

Therefore the effort by any bank to pursue another bank's customers will only be undertaken if there is a belief that enough of these customers will change and justify the cost of the pursuit. Unless PCA customers bother to move, then banks don't have to bother to be better.

If the Which? press release is an indication that customers are beginning to change, then the banks (especially the 'big four') need to start understanding the needs and opinions of their customers in a way that they have never had to before. If the rate of switching were to increase significantly it is unlikely that location would remain the key factor in choosing a PCA supplier. Sadly, as the above analysis shows, when customers do move the current key factor is location and thus the status quo is, to a large part, reinforced.

When customers begin to show a hunger for change then the banks will need to gain an appetite for improvement. Customers who are willing to change give banks the reason to bother to be better.

References

- British Banker’s Association quoting FSA, December 2001.

- http://www.moneyfacts.co.uk/.

- Vulnerable consumers and financial services, the report of the DGFT’s inquiry, January 1999.

- http://www.moneyfacts.co.uk/.

- Group Strategic Plan 2000-2002, quoted in Competition Review 2001.

- Abbey National submission to the Competition Commission 2001.

- Consumers' Association, Evidence No. 61 (extract from table) to the House of Commons, Treasury Select Committee Fifth Report published July 2002

- Competition in UK Banking: A Report to the Chancellor of the Exchequer, Cruickshank March 2000

- Shiv S Mathur and Alfred Kenyon, Creating Value: Shaping Tomorrow’s Business, Butterworth-Heinemann, 1997, pages 161-179.

- Keynes, John Maynard. 1923. A Tract on Monetary Reform. Vol 4, Chapter 3.

- The Collected Works of John Maynard Keynes, IV, (London: Macmillan, 1971). "In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is long past the ocean is flat again."

- Nobel Laureate in Economics 2002, for having integrated insights from psychological research into economic science, especially concerning human judgment and decision-making under uncertainty.

- Kahneman & Tversky, "Prospect Theory: An Analysis of Decision Under Risk" (Econometrica 47, 263-291) 1979.

- 1 September 2002 “Big 4 banks still trail behind smaller competitors on customer service”

Stephen Martin is the head of Z/Yen Aspect. He was previously the Marketing Director of Reliance Security, of OKI Systems (UK) and a Managing Consultant at Frank Lynn and Associates. Z/Yen Aspect is the Intelligence Division of Z/Yen and specialises in helping organisations to understand their complex customers. Stephen has been exploring customer behaviour to increase company value for 15 years and has applied this experience in almost every business sector where complex customer behaviour is evident.

Michael Mainelli originally did aerospace and computing research, before moving to finance. Michael was a partner in a large international accountancy practice for seven years before a spell as Corporate Development Director of Europe's largest R&D organisation, the UK's Defence Evaluation and Research Agency, and becoming a founder of Z/Yen in 1994. Michael has been advising banks around the world for over 15 years on strategy, systems, finance and risk, as well as many industrial companies. (Michael_Mainelli@zyen.com) Z/Yen Limited is a risk/reward management firm working to improve business performance through better decisions.

Z/Yen Limited undertakes strategy, finance, systems, marketing and organisational projects in a wide variety of fields (www.zyen.com), such as recent projects managing development of a client's stochastic perception engine or benchmarks of transaction costs across 25 European investment banks. Z/Yen's humorous risk/reward management novel, 'Clean Business Cuisine: Now and Z/Yen', awarded Sunday Times Book of the Week in 2000, has been described as "very tongue in cheek and very funny but also strangely enlightening" by Business Age.

[A version of this article originally appeared as "Why Bother to Be Better? Strategically Stagnant Personal Current Accounts", Journal of Strategic Change, Volume 12, Number 4, John Wiley & Sons (June-July 2003) pages 209-221.]