Is Small Beautiful? Investment In Smaller Quoted Companies

By

Professor Michael Mainelli

Published by Balance Sheet, The Michael Mainelli Column, Volume 11, Number 1, MCB University Press, pages 68-71.

As is well-known, all available information is incorporated into market prices. Or is it? A continuing puzzle is the difficulty of encouraging investment in smaller quoted companies (SQCs). The puzzle is global. It seems as if every country laments the state of SQC equity - too little institutional attention, onerous shareholder protections imposed by regulators, too little liquidity, poor management of investors and much, much more. However, if risk-adjusted rates of return on capital (RAROC) are taken into account, then surely rational investors will invest appropriately in SQCs?

By the 1970's there was clear, persistent under-pricing of SQCs, i.e., with few exceptions studies in several countries showed a small company premium persistent over several decades. This flies in the face of the fact that RAROC should level out, according to the Capital Asset Pricing Model (CAPM). Academic work had sought to identify the source of the premium. The most promising avenues had been either that small companies were inherently riskier in some way that standard measures of market risk (beta) did not capture or that transaction costs were higher for small companies (known to be true) and that if these costs were factored in then the superior returns would disappear. However, in practically all cases the premium reversed in the late 1980s or early 1990s, a small company discount, which also violates CAPM.

A number of inconclusive or contradictory studies shed little light on the premium/discount situation. A number of research avenues remain, perhaps:

- Small companies are inherently more risky in some way not captured by standard measures and the last decade has just been bad for smaller companies. In the UK, this is supported by evidence that the dividend performance of SQCs was superior to larger companies until the late 1980s and has since been inferior.

- Governance issues have become more prominent. Small companies are subject to greater governance risk because they tend to be less researched and have more concentrated management, increasing asymmetric information to the disadvantage of investors. In previous decades, governance differences between large and small companies were less marked and small companies were not penalised.

- Globalisation of investment and expansion in available asset types have created other opportunities for investors. Growth in passive investment suggests that investors can obtain the same risk/diversification benefits from foreign stocks or other assets such as derivatives that they used to obtain by diversifying into SQCs. Investors can now assemble portfolios with similar risk profiles to small cap stocks using other assets.

- Given massive adjustments in larger listed firms during 2001 and 2002 (e.g. Enron, WorldCom, et alia), the increased risk of larger firms needs updating and that the smaller company discount has returned to a premium. Thus, updated analysis would look over a longer time horizon and re-confirm the Small Company Premium.

- Poor access to structured debt has confused the analysis of equity. As SQCs have poor access to bond markets, often relying on overdrafts as a primary debt instrument, directly comparative analysis with larger quoted companies may be flawed.

- The small company premium was heavily biased by a small number of star performers. Everyone knows small companies that have become giants, but most small companies are either small companies that remain small or large companies that have become small. Refined segmentation analysis of SQCs might vindicate RAROC and CAPM by categorising these rapidly rising stars separately from the relatively static background of most SQCs.

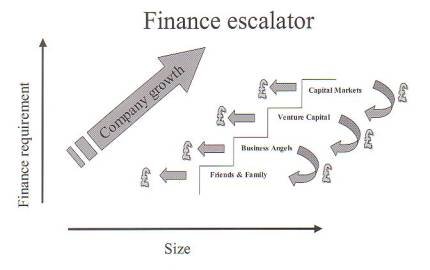

Part of the problem may well be that the risk in SQCs, as measured by volatility of returns, is confined to short periods. A well-respected view is that SQCs proceed up the following finance escalator:

“Bridging the equity gap: a new proposal for virtual local equity markets”, Tim Mocroft, Centre for the Study of Financial Innovation, Publication Number 47, January 2001.

However, these views, while neatly categorising organisations and placing them on a structured path, may not reflect reality. Perhaps SQCs have stable returns, punctuated infrequently by short periods of high volatility and, sometimes, high returns (related to point 6 above). If so, this supports further, but highly technical, research.

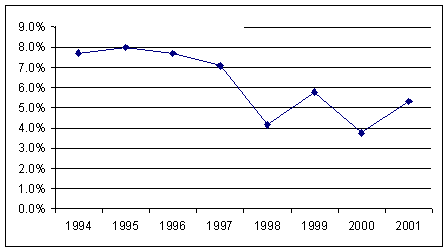

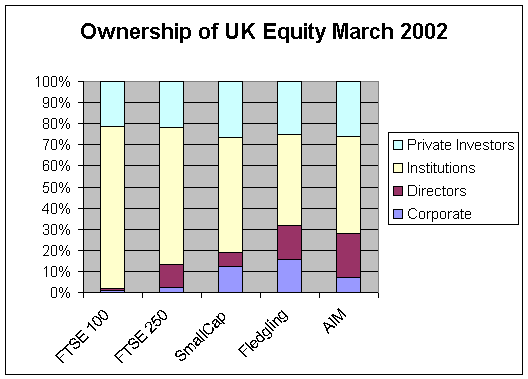

One study, "Institutional Investment and Trading in UK Smaller Quoted Companies", published by the Quoted Companies Alliance in October 2002 [available from http://www.qcanet.co.uk/publications/other/Research%20Report.pdf - this author was one of the contributors], is an interesting source of facts (as well as the diagrams in this paper). This study confirms that SQC investment is decreasing as a proportion of overall investment.

Proportion of UK Equity Funds Invested in SQCs 1994-2001

Although investment in SQCs has nearly tripled over the seven years from 1994 to 2001 - the proportion invested in SQCs has fallen. This overall view obscures a complex shift in investment - a strong decline in SQC investment by pension funds and unit trusts, partially offset by a strong increase from investment trusts. So a snapshot of overall equity ownership shows that, assuming RAROC was broadly equal, institutions are under-weighted in SQCs (and SQC directors are over-exposed to their own firms). Small may be pretty, but it's not beautiful to pension funds and unit trusts.

For a programme of recommendations to improve the position of SQCs in the UK, do investigate www.qcanet.co.uk. However, for the purposes of this article, the key issue is, if markets seem irrational, then where are the opportunities? Well, the opportunities seem to lie in at least three areas, for institutional investors, national economies and new investment structures.

Individual institutional investors should assure themselves that this apparent under-weighting in SQCs is justifiable. Agreed, SQCs require more effort for the sums involved, have lower liquidity, etc. But superior returns are only achieved by challenging received wisdom. The probable return of the small company discount and evident under-weighting mean that larger funds should re-examine their structures. There is the possibility that some synthetic structures, designed to achieve comparable, more liquid returns, do not accurately reflect inherent risks such as currency, demographic change or concentration. This might justify more direct SQC investment. A potential source of liquidity correction (one of the great ill-defined bugbears for institutions) may be coming from crossing networks. A landmark study of the liquidity advantages of "invisible" trading versus "transparent" trading must be on the horizon.

At a national policy level there are at least two big issues - appropriate allocation of assets to generate returns and employment. Appropriate allocation of assets is confused by taxation (stamp duty, differential corporation tax rates, interaction between corporation taxes, dividends and personal taxes, etc.), regulation (listing rules, publication of trade information, pension fund restrictions, etc.), trading systems and market structures, as well as the more important underlying fundamentals of the micro-economics within which SQCs operate (e.g. labour laws, housing markets, Customs & Excise regulations, public education, transportation infrastructure). A level playing field for appropriate investment decisions will be a long time coming. Nevertheless, SQCs translate into votes today. SQCs employ some 2 million people in the UK and account for almost 10% of private sector employment. SQCs cannot be seen to be disadvantaged, despite the transaction cost for government of working with them. Government must continue to remove obstacles to the appropriate allocation of investments in all classes, i.e. asset neutral regulation. A tall order, but material to long-term economic growth.

It is curious that new investment structures have not sprung up more rapidly, yet there are initiatives underway. On equity, reduced information costs are beginning to improve access to capital for SQCs and pre-SQCs, e.g. AngelBourse. There is also discussion of new debt structures, e.g. aggregated SQC debt as a securitised investment, as well as complementary products which may permit more tailored approaches, such as the rise of credit derivatives. SQCs in national economies, e.g. the UK, are competing globally with investments showing similar, or better, risk/reward ratios internationally. SQCs must market themselves harder, taking advantage of the geographic risk management bias their local institutions have over foreign institutions. However, there remains an open gap for savvy institutions that want to help with novel structures for debt and equity securitisation and placement.

Small seems to have been beautiful for less than two decades - part of the 1980's and part of the 1990's. In an increasingly well-priced world, small company premia should not exist. SQCs are a sector that should reward attention. Perhaps many of the obstacles are really canny smokescreens spread by specialists in SQCs to keep out the bigger institutions, and will be revealed as such. Perhaps the bigger institutions are too inefficient to handle SQCs, and need to change their cost structures. In an increasingly well-priced world, small should be as beautiful as large, and no more.

Michael Mainelli, FCCA, originally did aerospace and computing research, before stooping to finance. Michael was a partner in a large international accountancy practice for seven years before a spell as Corporate Development Director of Europe's largest R&D organisation, the UK's Defence Evaluation and Research Agency, and becoming a director of Z/Yen (Michael_Mainelli@zyen.com).

Z/Yen Limited is a risk/reward management firm working to improve business performance through better decisions. Z/Yen undertakes strategy, finance, systems, marketing and organisational projects in a wide variety of fields (www.zyen.com), such as recent projects developing a stochastic risk/reward prediction engine and benchmarking of transaction costs across 25 European investment banks. Michael's humorous risk/reward management novel, "Clean Business Cuisine: Now and Z/Yen", written with Ian Harris, was published in 2000; it was a Sunday Times Book of the Week and even Accountancy Age described it as "surprisingly funny considering it is written by a couple of accountants".

[A version of this article originally appeared as "Is Small Beautiful? Investment in Smaller Quoted Companies", Balance Sheet, The Michael Mainelli Column, Volume 11, Number 1, (March 2003) pages 68-71.]